As a Product Manager with over seven years of experience in tech and cloud services, I’ve seen countless workflows that look perfect on a whiteboard but crumble under the weight of real-world complexity. Recently, I had the opportunity to evaluate how enterprise-grade modeling tools can bridge the gap between high-level conceptual designs and production-ready business processes.

Using a retail banking loan origination scenario as my test case, I explored how Visual Paradigm handles the transition from a simple “idea” diagram to a robust, compliant, and automated BPMN 2.0 workflow. Below is my comprehensive review of the process evolution and the tooling that makes it possible.

Introduction: The Gap Between Theory and Practice

In product management, we often start with a “Happy Path”—a simplified view of how a user interacts with our system. However, financial services demand more than just a happy path; they require rigorous risk control, regulatory compliance, and fault tolerance.

The challenge I addressed was transforming a basic, conceptual loan request model into an enterprise-ready Loan Origination and Approval Process. This wasn’t just about drawing boxes and arrows; it was about enforcing business rules, separating duties, and ensuring that every decision point was auditable. Here is how the process evolved and how Visual Paradigm facilitated this transformation.

Case Study: Real-World Loan Origination and Approval Process (v2.0)

Executive Summary

Manual loan processing creates long wait times, operational errors, and compliance risks. This case study analyzes the modernized Business Process Model and Notation (BPMN 2.0) workflow engineered to automate, secure, and accelerate a retail banking loan lifecycle. By establishing clear cross-functional boundaries and rule-based gateways, this workflow transforms a high-risk financial process into a scalable, auditable, and customer-centric digital operation.

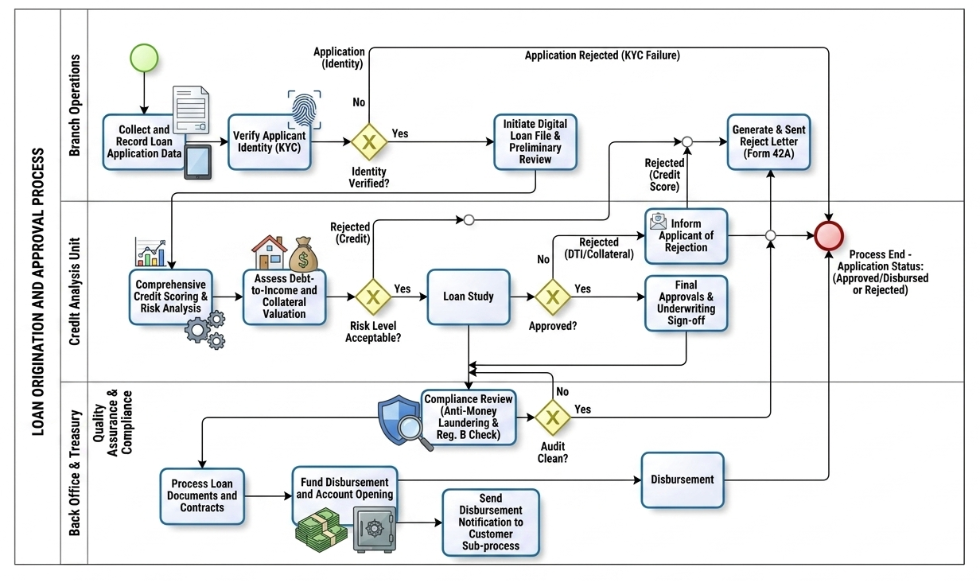

The “Who”: Operational Roles & Swimlanes

The BPMN diagram organizes the workflow into three distinct vertical swimlanes within the overall Loan Origination and Approval Process pool. This ensures clear ownership and separation of duties:

-

Branch Operations: The customer-facing front office. They handle initial intake, identity verification (KYC), and final customer communications regarding rejection.

-

Credit Analysis Unit: The specialized analytical hub. Risk managers and automated credit models evaluate financial viability, collateral value, and overall debt-to-income ratios.

-

Back Office & Treasury (with Quality Assurance & Compliance): The operational engine and governance checkpoint. This group handles regulatory verification (AML/Reg. B), contract execution, funding allocation, and digital distribution.

The “Why”: Business Value & Objectives

Traditional lending processes suffer from visibility silos and manual bottlenecks. This structured BPMN model solves these systemic issues by targeting three core goals:

-

Enforce Compliance & Risk Control: Automated gateways guarantee that identity checks (KYC) and Anti-Money Laundering (AML) screenings cannot be skipped or bypassed.

-

Reduce Time-to-Decision: By routing the application to a “Digital Loan File” immediately after KYC, the Credit Analysis unit can run risk scoring and collateral valuations concurrently.

-

Improve Customer Experience: Clear endpoints ensure that rejected applicants receive legally compliant notices (Form 42A) instantly, while approved applicants experience rapid funding turnaround.

The “How”: Step-by-Step Process Execution

1. Intake and Identity Verification (Branch Operations)

-

Start: The process triggers when a customer submits a loan request.

-

Collection: Branch agents gather application data via digital tablets.

-

KYC Gateway: A biometric fingerprint/ID scan runs automatically. If identity verification fails (No), the path routes directly to a rejection letter generation task, ending the process. If it succeeds (Yes), a digital loan file initiates.

2. Risk Assessment & Underwriting (Credit Analysis)

-

Dual-Track Analysis: The file moves to Credit Analysis, where parallel tasks run automated credit scoring, risk modeling, debt-to-income (DTI) calculations, and collateral valuations.

-

Risk Level Gateway: An exclusive gateway evaluates the combined credit/risk profile. High-risk profiles route immediately to a rejection notification task.

-

Loan Study & Underwriting Sign-Off: Acceptable files undergo a formal loan study. A final gateway determines if underwriting criteria are met. If rejected due to DTI or poor collateral, it routes to the rejection track. If approved, it receives formal underwriting sign-off.

3. Compliance and Funding (Back Office & Treasury)

-

The Compliance Firewall: Approved files are sent to the Quality Assurance sub-lane for an automated Compliance Review (AML and Regulation B checks).

-

Audit Gateway: If the audit exposes any red flags (No), the file is routed backward to the rejection track. If clean (Yes), document processing begins.

-

Disbursement & Closing: Back Office signs and processes legal contracts, establishes the new account, and triggers treasury funds to disburse the loan amount. A sub-process concurrently sends a digital confirmation to the client.

-

End: All paths—whether leading to a disbursed loan or a generated rejection letter—converge cleanly into a single End Event, marking the file as officially closed.

Key BPMN Concepts Demonstrated

[Start Event] ──> [Task / Activity] ──> [Exclusive Gateway (X)] ──> [End Event]

│

└── (Alternative Path) ──>

-

Pools and Swimlanes: Represent organizational boundaries (the Bank) and individual departmental accountabilities (Branch, Credit, Back Office).

-

Tasks (Rectangles): Represent atomic units of work. The diagram distinguishes between user/manual data entry (tablets), automated service tasks (biometric/system checks), and complex sub-processes (notifications).

-

Exclusive Gateways (Diamonds with an ‘X’): Act as structural decision points. They evaluate strict business logic (Yes/No, Pass/Fail) and route the process token down exactly one mutually exclusive path.

-

Sequence Flows (Solid Arrows): Direct the exact chronological and logical progression of data and activities from start to finish.

Process Comparison: Conceptual vs. Real-World Execution

When moving from a high-level conceptual model to an enterprise-ready production environment, business processes must evolve to handle complex business rules, strict regulatory compliance, and deeper automation. Below, we analyze how each phase of the original Loan Request process scales into a comprehensive, real-world Loan Origination and Approval workflow.

1. Front-Office Intake and Verification Phase

In the initial model, this phase is represented as a simple two-step sequence: recording application data followed by verifying applicant information.

In a production environment, this is expanded to ensure data integrity and strict risk control at the very first point of contact:

-

Digital Data Capture: The manual registration task evolves into an automated asset collection process using digital interfaces, minimizing data entry errors.

-

Biometric KYC Validation: Generic applicant verification is replaced by a formal, system-integrated Know Your Customer (KYC) gate. The process introduces a dedicated Identity Verified? exclusive gateway.

-

Immediate Fail-Safe Routing: If identity validation fails, the process completely bypasses downstream underwriting systems and routes directly to the rejection track, saving operational costs and reducing fraud risks.

2. Credit Factory and Advanced Underwriting Phase

The original diagram relies on a single Loan Study task and a basic Loan Approved? decision gateway to determine the viability of a loan request.

In practice, financial risk management requires multi-layered analytical tasks running concurrently to assess exposure:

-

Concurrent Risk Architecture: Before a formal loan study begins, a real-world system executes parallel tracks for Comprehensive Credit Scoring & Risk Analysis alongside a physical or digital Debt-to-Income & Collateral Valuation.

-

Risk Level Gateway: An additional exclusive gateway (Risk Level Acceptable?) filters out unviable applications early in the credit cycle, ensuring underwriters only dedicate time to applications that meet minimum risk appetites.

-

Underwriting Sign-Off: The final approval gateway is supported by a concrete Final Approvals & Underwriting Sign-off task, creating a definitive audit trail for credit decisioning.

3. Back-Office Compliance and Disbursement Phase

The conceptual workflow finishes abruptly by routing an approval straight to a disbursement task. A professional banking architecture demands a final gatekeeper layer to ensure legal and treasury compliance before any capital leaves the institution.

-

The Compliance Firewall: A dedicated Quality Assurance & Compliance sub-lane is injected directly prior to funding. The approved application must pass an independent Compliance Review evaluating Anti-Money Laundering (AML) and Regulation B constraints.

-

Audit Gateway: A clean compliance audit (Audit Clean?) acts as the absolute green light for treasury. If compliance fails, the application is securely rerouted back to the rejection workflow.

-

Multi-Channel Closing: Once verified, the final Disbursement phase breaks down into parallel automated tasks: formal legal contract processing, account generation, capital funding, and an asynchronous customer notification sub-process.

Tooling Review: Visual Paradigm for Enterprise BPMN

To model the complex workflow described above, I utilized Visual Paradigm. It provides a robust, enterprise-grade modeling suite fully compliant with the BPMN 2.0 standard. Designed to bridge the communication gap between business analysts and technical implementation teams, it offers comprehensive tools for drawing, analyzing, and animating business processes.

Core Modeling Features

-

Full BPMN 2.0 Element Support: Access the complete palette of standards-compliant elements including all specialized Events (Message, Timer, Signal, Error), Activity sub-types (User, Service, Script, Call Activities), Gateways, and Data Objects.

-

Process Drill-Down (Hierarchical Sub-Processes): Create a highly readable “parent” process and link it to an entirely separate, lower-level child diagram. This allows users to easily collapse or expand sub-processes to toggle between macro views and granular task details.

-

Resource Modeling & Swimlanes: Organize workflow layouts across complex organizational structures by adding horizontal or vertical Pools and dynamic Swimlanes.

AI & Automation Innovations

-

AI Text-to-Diagram Generation: Convert plain-English written descriptions of a workflow instantly into interactive, standards-compliant business process diagrams.

-

Resource Co-Pilot: Speed up manual construction using contextual menus that automatically suggest the next logical BPMN shape or connecting flow object upon hovering.

Advanced Visualization & Integration

-

Process Simulation & Animation: Play through the design using built-in diagram animations to visually trace token progression, helping teams find logic errors or deadlocks before coding.

-

Cross-Standard Mapping: Seamlessly link business process diagrams directly to technical specifications such as UML sequence diagrams, Entity-Relationship Diagrams (ERDs), User Stories, or corporate enterprise architecture components (TOGAF/ArchiMate).

-

Enterprise Reporting: Instantly compile finalized diagrams and their underlying data definitions into professional, automated compliance documentation.

Conclusion: Bridging the Gap with Precision

Transitioning from a conceptual loan request to a fully compliant origination system is not merely a design exercise—it is a strategic imperative. As demonstrated in this case study, the addition of rigorous KYC gates, parallel risk analysis tracks, and mandatory compliance firewalls transforms a fragile process into a resilient operational engine.

Visual Paradigm proved to be an indispensable partner in this journey. Its ability to handle hierarchical sub-processes allowed us to keep the high-level view clean while drilling down into the complexities of credit scoring and AML checks. Furthermore, the AI-driven features and simulation tools reduced the time spent on iterative corrections, allowing our team to focus on optimizing business logic rather than wrestling with diagram syntax.

For product managers and business analysts tasked with digitizing complex financial workflows, adopting a tool that supports both strict BPMN compliance and agile visualization is key to delivering secure, efficient, and customer-centric solutions.

References

- Visual Paradigm Features Overview: A comprehensive overview of the core capabilities and modules available in the Visual Paradigm suite.

- BPMN Diagram and Tools: Detailed information on specific BPMN modeling tools, including element support and diagramming features.

- From Narrative to Diagram: How Visual Paradigm’s AI BPMN Generator Transforms Process Modeling Workflows: An article explaining how AI technology converts text descriptions into visual business process diagrams.

- What is BPMN?: A foundational guide explaining the Business Process Model and Notation standard and its importance.

- BPMN Guide: General resources and guides for understanding and implementing BPMN standards.

- BPMN Guide (Additional Resources): Further documentation on BPMN elements and best practices.

- BPMN Diagram and Tools (Detailed): In-depth look at the specific tools for creating and managing BPMN diagrams.

- Understanding BPMN: A Comprehensive Overview: A detailed guide from the Visual Paradigm knowledge base covering BPMN concepts.

- Swimlanes and Pools Guide: Specific instructions on using swimlanes and pools to organize process responsibilities.

- Visual Paradigm YouTube Tutorial: Video demonstration of BPMN modeling features and tips.

- AI BPMN Generator Guide: Additional insights into the AI-powered diagram generation capabilities.

- BPMN and Enterprise Architecture Integration: Information on linking BPMN diagrams with other enterprise architecture standards.

- Visual Paradigm Feature Set: Overview of the broader feature set including integration capabilities.

- Enterprise Reporting Features: Details on generating automated reports and documentation from process models.